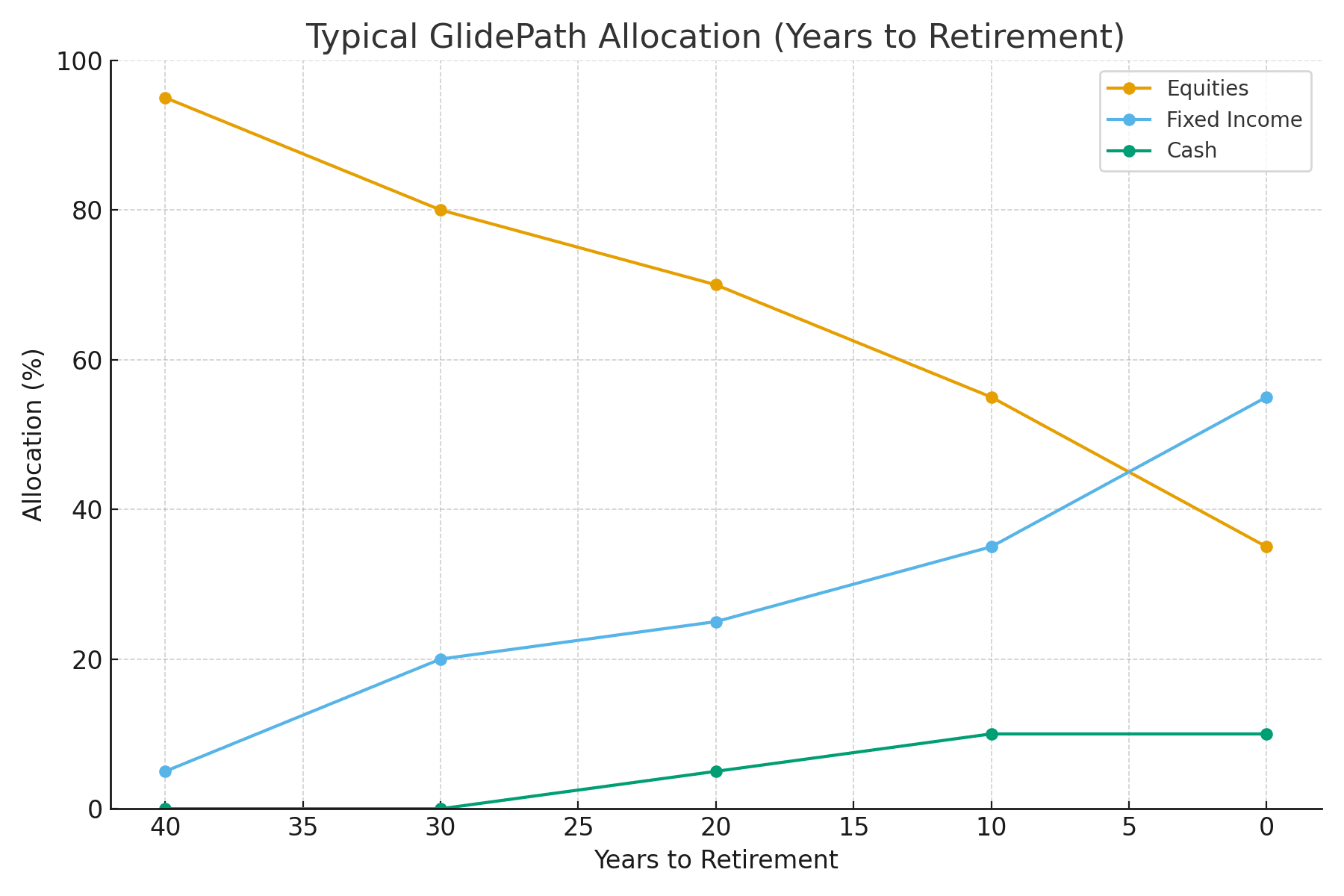

Typical GlidePath Allocation

How a portfolio shifts from growth to preservation as retirement approaches.

{kind=link}

Illustrative only. Actual allocations should reflect risk tolerance, liquidity needs, and client objectives.

Partners & Carriers We Work With

Independent access to multiple leading insurers across Canada.

Visit Medavie Blue Cross

Visit Assumption Life

Visit Assumption Life

Visit Foresters Financial

Visit Foresters Financial

Visit Humania Assurance

Visit Humania Assurance

Visit Canada Protection Plan

Visit Canada Protection Plan

Visit Industrial Alliance

Visit Industrial Alliance

Visit Sun Life Financial

Visit Sun Life Financial

Visit Desjardins Financial Security

Visit Desjardins Financial Security

Visit Canada Life

Visit Canada Life

Visit Empire Life

Visit Empire Life

Visit RBC Insurance

Visit RBC Insurance

Visit Equitable Life of Canada

Visit Equitable Life of Canada

Visit Manulife Financial

Visit Manulife Financial

Visit Beneva Insurance

Visit Beneva Insurance

Visit Green Shield Canada

Visit Green Shield Canada

Visit Assumption Life

Visit Assumption Life

Visit Foresters Financial

Visit Foresters Financial

Visit Humania Assurance

Visit Humania Assurance

Visit Canada Protection Plan

Visit Canada Protection Plan

Visit Industrial Alliance

Visit Industrial Alliance

Visit Sun Life Financial

Visit Sun Life Financial

Visit Desjardins Financial Security

Visit Desjardins Financial Security

Visit Canada Life

Visit Canada Life

Visit Empire Life

Visit Empire Life

Visit RBC Insurance

Visit RBC Insurance

Visit Equitable Life of Canada

Visit Equitable Life of Canada

Visit Manulife Financial

Visit Manulife Financial

Visit Beneva Insurance

Visit Beneva Insurance

Visit Green Shield Canada

Visit Green Shield Canada

Visit Medavie Blue Cross

Visit Assumption Life

Visit Foresters Financial

Visit Humania Assurance

Visit Canada Protection Plan

Visit Industrial Alliance

Visit Sun Life Financial

Visit Desjardins Financial Security

Visit Canada Life

Visit Empire Life

Visit RBC Insurance

Visit Equitable Life of Canada

Visit Manulife Financial

Visit Beneva Insurance

Visit Green Shield Canada

Visit Assumption Life

Visit Foresters Financial

Visit Humania Assurance

Visit Canada Protection Plan

Visit Industrial Alliance

Visit Sun Life Financial

Visit Desjardins Financial Security

Visit Canada Life

Visit Empire Life

Visit RBC Insurance

Visit Equitable Life of Canada

Visit Manulife Financial

Visit Beneva Insurance

Visit Green Shield Canada

Logos are trademarks of their respective owners and are used for identification only.